Global financial crisis fears grow as bond yields hit 1998 levels and Bitcoin drops below $80,000

Is a worldwide 2008-style economic crash nigh? And do present circumstances resemble the early levels of a broader world financial crisis pushed by debt prices, inflation stress, and constrained coverage responses?

Those questions have develop into tougher to dismiss as a result of the stress factors are stacking within the unsuitable order: high sovereign yields, high public debt, an energy shock, sticky inflation, and stretched asset valuations.

The world has echoes of 2008, however the coverage setting is totally different. Banks are higher capitalized than they have been earlier than the worldwide financial crisis, and the Federal Reserve’s newest financial-stability work nonetheless factors to areas of resilience in family and financial institution steadiness sheets.

Any 2020 analogy additionally breaks down: governments and central banks may then flood the system with assist whereas inflation was muted.

The setup is totally different as a result of the rescue tradeoff is costlier. Global public debt stood at just below 94% of GDP in 2025 and is projected to succeed in 100% by 2029 within the IMF’s April Fiscal Monitor.

The World Bank is warning that the Middle East conflict can push power, meals, fertilizer, and inflation increased. The Financial Stability Board has flagged sovereign bond markets, asset valuations, and non-public credit score as areas that want shut monitoring.

The result’s a reputable, cheap worst case, with inevitability nonetheless outdoors the proof.

Sovereign yields return to world financial crisis warning levels

[Editor’s Note: Intraday volatility was extremely high today, May 13. Snapshot used for this article was taken around 14.00 UTC]

The bond market is the place the query begins. Intraday government-bond information at this time, May 13, confirmed U.S. Treasurys at roughly 3.99%, 4.46%, and 5.03% throughout the 2-year, 10-year, and 30-year tenors.

U.Ok. gilts have been round 4.53%, 5.10%, and 5.78%. German Bunds have been close to 2.71%, 3.11%, and 3.63%. Japanese authorities bonds sat at round 1.40%, 2.59%, and 3.82%.

The historic comparability is important right here. Nasdaq beforehand marked U.S. 2-year yields on the highest since 2007, after they reached 4%.

U.Ok. 2-year gilts are on the highest levels since June 2008, whereas U.Ok. 10-year yields are close to 18-year highs, and 30-year gilts are close to levels related to 1998.

Germany’s 10-year Bund is near its highest degree since May 2011, through the eurozone debt crisis. Japan’s 10-year yield has reached levels final seen in 1997, with the 2-year yield at levels final seen in 1995.

China is the exception. Its 10-year authorities bond yield was round 1.74% on May 13, with the 2-year close to 1.27% and the 30-year close to 2.24%, in keeping with Trading Economics.

That curve factors to a unique development and value backdrop, splitting the story into high-yield stress in developed markets and low-yield development stress in China.

The developed-market facet nonetheless carries the larger fiscal drawback. The OECD’s 2026 debt work reveals heavy sovereign borrowing and refinancing wants throughout its member economies.

Higher yields roll into auctions, coupon prices, and political selections over time. The longer the lengthy finish stays elevated, the extra the market forces governments to decide on between increased curiosity payments, lowered spending flexibility, and bigger deficits.

In 2008, aggressive financial rescue and balance-sheet assist helped stabilize the financial system. In 2020, fiscal and financial enlargement bridged a sudden collapse in exercise.

In 2026, the debt inventory is greater, long-end yields are increased, inflation threat is seen, and an power shock is already inside the information.

Hormuz turns oil threat into coverage threat

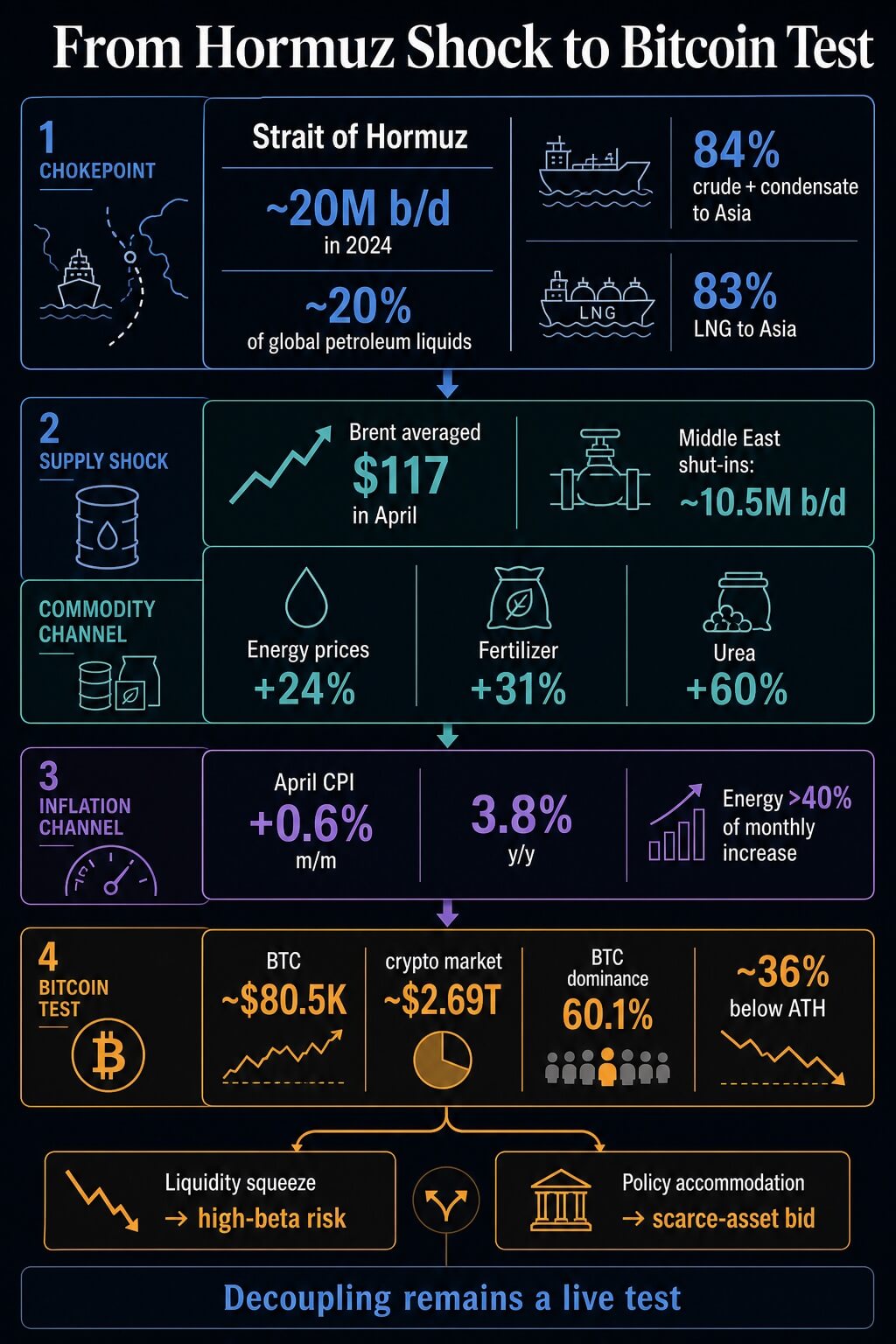

The Strait of Hormuz is the principle stress level as a result of it turns a regional battle into a worldwide price shock. The U.S. Energy Information Administration estimates that roughly 20 million barrels per day moved by means of the strait in 2024, equal to about 20% of world petroleum liquids consumption.

The company additionally estimated that 84% of crude oil and condensate and 83% of LNG shifting by means of Hormuz went to Asian markets that 12 months.

The present shock has moved into official value and provide forecasts. In its May 2026 Short-Term Energy Outlook, the EIA described Hormuz as successfully closed to delivery site visitors, mentioned Brent averaged $117 per barrel in April, and assessed Middle East manufacturing shut-ins round 10.5 million barrels per day that month.

The company assumes flows start to renew from late May or early June, however that assumption is itself one of many dwell threat variables.

The World Bank’s April Commodity Markets Outlook places the macro channel in plain phrases. Energy costs are projected to surge 24% this 12 months, Brent is forecast at $86 per barrel within the baseline, and a severe-disruption situation may push Brent as high as $115.

Fertilizer costs are projected to rise 31%, pushed by a 60% leap in urea. The identical report warns that increased commodity costs will raise inflation and weaken development, particularly in creating economies that have already got restricted fiscal buffers.

The U.S. information already present a part of that pass-through. The Bureau of Labor Statistics mentioned April CPI rose 0.6% on a seasonally adjusted month-to-month foundation and 3.8% over the 12 months earlier than seasonal adjustment.

Energy accounted for greater than 40% of the month-to-month enhance.

That is the mechanism that makes the crash query credible. A shorter shock can nonetheless maintain inflation expectations agency sufficient to sluggish fee cuts whereas debt-service prices proceed to climb.

If development weakens on the identical time, the coverage alternative turns into ugly: defend inflation credibility or defend financial stability.

| Trigger | Transmission path | Release valve |

|---|---|---|

| Higher sovereign yields | Debt-service prices rise as governments refinance | Debt maturities stagger the influence over time |

| Hormuz disruption | Oil, LNG, fertilizer and delivery prices feed inflation | Rerouting, demand adjustment and resumed flows can soften the primary shock |

| Sticky inflation | Central banks have much less room to chop into market stress | Weak development can nonetheless power lodging later |

| High valuations and leverage | Risk belongings have much less margin for unhealthy information | Bank and family steadiness sheets nonetheless present resilience |

| Bitcoin decoupling take a look at | BTC both trades as scarce collateral or high-beta threat | Recent divergence is early and nonetheless wants affirmation |

Why markets have much less coverage assist than earlier than the worldwide financial crisis

The equity-market stress is that threat belongings can look calm even whereas the bond market is repricing the coverage backdrop. The Fed’s May Financial Stability Report mentioned ahead fairness price-to-earnings ratios remained within the higher vary of their historic distribution.

Corporate bond spreads have been nonetheless low by longer-run requirements. Hedge fund leverage remained close to all-time highs and was concentrated among the many largest funds.

That combine is a cushion drawback. The identical Fed report mentioned market contacts most regularly cited geopolitical dangers, an oil shock, non-public credit score, and persistent inflation as salient dangers to financial stability.

The FSB made an analogous level in April, saying the Middle East battle had already created a considerable world financial shock, with market reactions seen in power costs and authorities bond yields.

That is the collision traders have to look at throughout coverage conferences, auctions, and liquidity circumstances. Markets can soak up high charges when development is powerful, inflation is falling, and fiscal financing appears to be like manageable.

They can soak up oil shocks when central banks can look by means of the value spike. They can soak up high public debt when borrowing prices are pinned down. The present setup weakens every cushion without delay.

A crash turns into an inexpensive worst case if the sequence tightens: Hormuz retains power and fertilizer costs high; inflation stays sticky; central banks delay assist; long-end yields keep elevated; debt-service stress grows; threat belongings that had priced a tender touchdown reprice towards weaker development and tighter liquidity.

A calmer path can be attainable. If oil flows normalize, inflation eases, actual yields soften, and central banks can pivot towards development assist, the stress stack breaks earlier than it turns into systemic. That framing is conditional fragility.

That distinction is important for market timing. Sovereign stress tends to construct by means of auctions, refinancing calendars, credit score spreads, fairness multiples, and central-bank choices. It hardly ever publicizes itself by means of one clear set off.

That provides markets time to adapt, but it surely additionally means stress can maintain accumulating after the primary oil-price spike fades. A soft-landing commerce can survive one shock; the tougher take a look at is whether or not it survives a number of without delay, with every channel limiting the coverage reply to the following.

Bitcoin turns into the macro take a look at throughout world financial crisis fears

Bitcoin sits on the finish of this chain as a result of it’s now a part of the macro learn.

Bitcoin traded round $80,500 on May 13, earlier than scorching PPI pushed it below $80,000, whereas the broader crypto market stood at round $2.69 trillion, and BTC dominance held at round 60.1%.

That leaves it nonetheless massive sufficient to be a macro asset, whereas its volatility retains it outdoors clean-shelter standing.

Recent CryptoSlate coverage has famous home windows when Bitcoin moved in a different way from U.S. equities amid oil, yield, and greenback stress on shares. Another CryptoSlate analysis framed the Hormuz shock as a fork for Bitcoin: both a liquidity squeeze that drags BTC again into high-beta collateral habits, or a policy-accommodation path that revives the scarce-asset commerce.

That is the sober method to deal with Bitcoin right here. Bitcoin’s file as a steady inflation hedge stays unproven. Its separation from threat urge for food stays incomplete.

Glassnode’s newest market pulse helps warning: bettering construction nonetheless wants affirmation amid macro stress from charges, oil, and liquidity.

A single unhealthy fairness session tells little. The take a look at is whether or not Bitcoin can maintain up if shares dump, yields keep high, the greenback corporations, and central banks hesitate to ease as a result of inflation remains to be being fed by power and meals prices.

If BTC holds that setting, the monetary-disorder narrative will get stronger. If it fails, the market could have handled it as one other threat asset with higher branding.

That leaves the crash query with a sensible reply. A 2008 replay stays an outdoor risk, and the declare of inevitability is just too robust.

However, the present setup is extra fragile as a result of the general public debt load is heavier, the inflation shock is actual, and the coverage response is extra constrained.

One value chart will inform solely a part of the story; the coverage alternative will carry the larger sign. If central banks prioritize inflation management whereas oil and debt-service prices maintain rising, financial markets will face better stress and not using a rescue.

If they shift towards financial stability, Bitcoin faces its clearest take a look at as a hedge towards coverage lodging and currency-credibility threat.

Either approach, the query has moved from alarmism to threat administration. What pulls it again from the brink is that a number of launch valves nonetheless exist:

- The shock is conditional. If Hormuz flows resume and oil normalizes, the inflation impulse weakens.

- Debt stress rolls by means of time. Refinancing calendars stagger the hit fairly than forcing one fast rupture.

- Balance sheets are stronger than 2008. The piece cites resilience in banks and households, which limits direct GFC-style contagion.

- Central banks nonetheless have optionality. They are constrained by inflation, however weak development or market stress can nonetheless power lodging later.

- Markets have warning indicators. Auctions, long-end yields, credit score spreads, liquidity, fairness multiples, and BTC’s habits give a sequence to watch.

The put up Global financial crisis fears grow as bond yields hit 1998 levels and Bitcoin drops below $80,000 appeared first on CryptoSlate.