Multicoin Exec Says GENIUS Act Will End Banks’ ‘Rip-Off’ of Retail Depositors with Low Rates

Multicoin Capital managing associate Tushar Jain has predicted that the GENIUS Act will set off a aggressive upheaval in retail banking, with main expertise corporations poised to problem conventional banks by providing stablecoin merchandise with superior yields and person experiences.

Jain argued that banks have lengthy exploited retail depositors by paying minimal rates of interest.

He foresaw that tech giants like Meta, Google, and Apple would quickly leverage their large distribution networks to supply stablecoins with higher returns, prompt settlement, 24/7 funds, and free transfers embedded instantly into broadly used apps and working techniques.

Banking Industry Fights Yield-Sharing as Deposit Flight Fears Mount

The banking sector has mounted an aggressive lobbying marketing campaign to forestall stablecoin platforms from providing aggressive yields to holders, regardless of the GENIUS Act’s prohibition making use of solely to issuers, not intermediaries.

Five main U.S. banking commerce organizations have urged Congress to close perceived “loopholes” that permit crypto exchanges to supply stablecoin yields by affiliate applications and advertising and marketing preparations, citing Treasury estimates of potential $6.6 trillion deposit outflows.

Citigroup analyst Ronit Ghose particularly warned that stablecoin curiosity funds might set off Nineteen Eighties-style deposit flight just like when cash market funds surged from $4 billion to $235 billion in seven years, draining conventional financial institution deposits.

During that interval, withdrawals exceeded new deposits by $32 billion between 1981 and 1982 as shoppers chased increased returns.

The American Bankers Association and the Bank Policy Institute argued that joint advertising and marketing preparations between issuers and exchanges might speed up deposit flight in periods of monetary stress.

However, the banking foyer’s place faces contradictions as main establishments concurrently discover stablecoin alternatives.

Citigroup CEO Jane Fraser confirmed the financial institution is “trying on the issuance of a Citi stablecoin” whereas growing tokenized deposit providers for company shoppers.

JPMorgan also launched JPMD deposit tokens for institutional blockchain funds and served as lead underwriter for Circle’s IPO.

Jain dismissed banking issues, noting that the prohibition on passing curiosity to stablecoin holders is “simply circumvented,” as evidenced by Coinbase’s yield-sharing with prospects.

Stripe CEO Patrick Collison reinforced this view, arguing that depositors “are going to, and will, earn one thing nearer to a market return on their capital.”

Given that common U.S. financial savings deposits yield simply 0.40%, whereas $4 trillion in financial institution deposits earn 0% curiosity, Collison’s level is well-taken.

Stablecoin Market Consolidation Faces Disruption From New Entrants

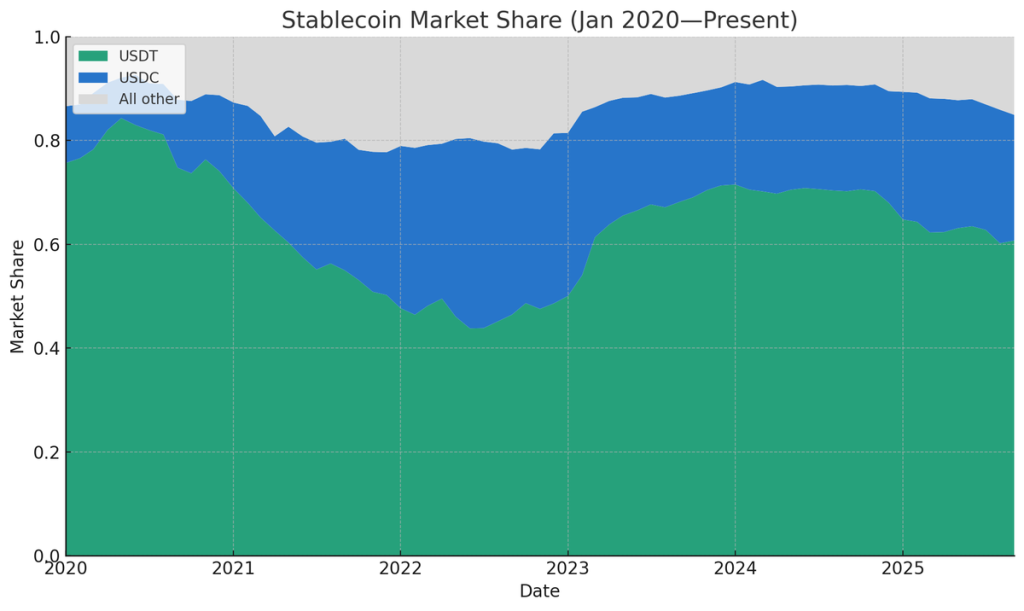

The long-standing Tether-Circle duopoly, which controls 86% of the $298 billion stablecoin market, faces mounting strain from new issuers providing yield-sharing preparations and customizable reserve constructions.

Venture capitalist Nic Carter argued that the dominance of the 2 main issuers has begun declining from its 91.6% peak in March 2024, pushed by intermediaries rolling their very own stablecoins to seize reserve yield relatively than surrendering income to 3rd events.

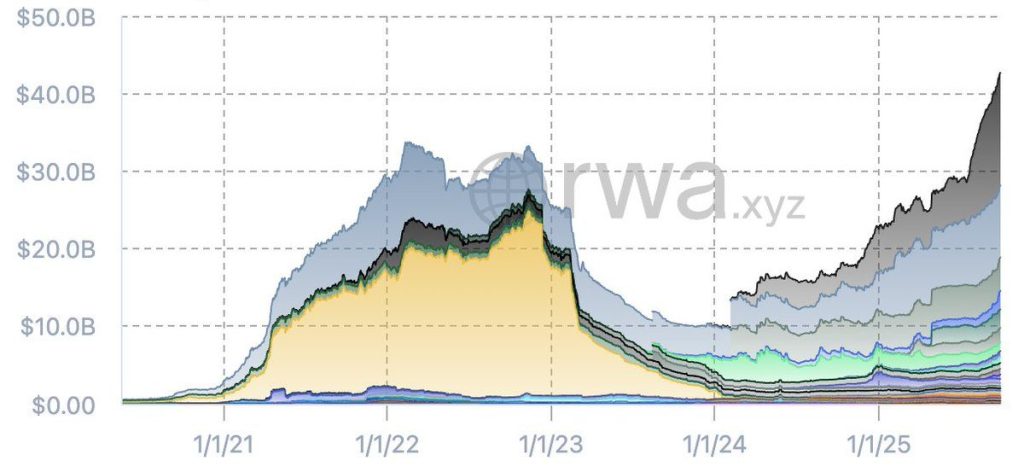

White-label issuance platforms, together with Bridge, Anchorage, Brale, M0, and Agora, have dramatically lowered fastened prices, enabling even seed-stage startups to launch their very own stablecoins.

Exchanges and fintechs now face sturdy incentives to internalize yield relatively than permitting Tether to earn roughly $35 million yearly on each $500 million in deposits whereas the middleman receives nothing.

Phantom pockets launched Phantom Cash, a Bridge-issued stablecoin with embedded earn and debit card functionalities.

Meet Phantom Cash

The energy of crypto

the convenience of money. pic.twitter.com/F7yL7sNxKd

— Phantom (@phantom) September 30, 2025

Similarly, Hyperliquid’s public bidding process for its stablecoin attracted proposals from Native Markets, Paxos, Frax, Agora, Sky, Curve, and Ethena.

The platform at the moment hosts $5.5 billion in USDC, representing 7.8% of the overall USDC provide, and goals to scale back its dependence on Circle whereas capturing reserve yield.

Ethena’s USDe has emerged as the largest success story of 2025, surging to a $14.7 billion provide by passing alongside yield from crypto-based trades.

Other yield-focused stablecoins, together with Ondo’s USDY, Maker’s SUSD, Paxos’ USDG, and Agora’s AUSD, have collectively gathered extra provide than in the course of the prior bull market cycle.

Carter famous that cross-chain swaps have turn out to be considerably extra environment friendly and cheaper, lowering community results that beforehand benefited main issuers.

According to him, many fintechs and neobanks now show person balances in generic “{dollars}” or “greenback tokens” relatively than USDC or USDT, guaranteeing redeemability in any stablecoin whereas managing reserves internally.

The Global Dollar consortium, launched by Paxos, contains Robinhood, Kraken, Anchorage, Galaxy, Bullish, and Nuvei, alongside over a dozen different companions.

Similarly, a report by Cryptonews means that JPMorgan, Bank of America, Citigroup, and Wells Fargo held early talks about creating their very own stablecoin consortium.

Carter predicted that banks will be a part of the stablecoin market as issuers, regardless of issues about deposit flight, noting that even sustaining a 50- to 100-basis-point margin might generate significant income from trillions of deposits.

The put up Multicoin Exec Says GENIUS Act Will End Banks’ ‘Rip-Off’ of Retail Depositors with Low Rates appeared first on Cryptonews.