Stablecoins Threaten to Disrupt U.S. Bank Deposits and Payments, Morningstar DBRS Warns

Stablecoins have quickly grow to be a central pillar of the digital asset economic system, now exceeding a mixed market capitalization of $230 billion as of mid-2025, in keeping with Morningstar DBRS.

The market is led by Tether (USDT) and Circle (USDC), with different gamers together with USDe, DAI, and FDUSD (see Exhibit 1). This progress has been fuelled by their stability — pegged to the U.S. greenback — and their means to perform as digital money inside the blockchain ecosystem.

The passage of the primary federal stablecoin laws on July 17 has additionally accelerated adoption. With regulation in place, U.S. banks are starting to discover launching their very own stablecoins, notes the company.

“Stablecoins supply effectivity and innovation within the monetary system, however additionally they pose each alternatives and dangers for banks,” Morningstar DBRS analysts wrote in a report revealed Tuesday.

How Stablecoins Work: Cheaper, Quicker, Smarter Cash

Morningstar explains stablecoins are designed to mix the reliability of fiat currencies with the effectivity of blockchain. Not like conventional fee rails — bank cards, ACH, or wire transfers — stablecoin transactions settle in seconds.

“Stablecoins are programmable cash,” Morningstar notes, highlighting their use in sensible contracts that mechanically execute monetary operations.

This has made them engaging for cross-border funds, e-commerce, and remittances. Main issuers like Tether, Circle, and PayPal again their cash with reserves of short-term U.S. Treasuries and money equivalents, guaranteeing stability and redeemability.

The effectivity benefit is stark: the place wire transfers can value as much as $50 and take days to settle, stablecoins transfer immediately with negligible charges. This dynamic is drawing customers away from banks’ legacy methods.

Dangers to U.S. Banks: Deposits and Funds at Stake

Morningstar warns that the rise of stablecoins poses actual dangers to U.S. banks’ core enterprise fashions. Essentially the most rapid concern is deposit flight.

If customers more and more maintain funds in stablecoins for rewards, comfort, or integration with decentralized finance, banks might lose the deposits that underpin their lending operations.

In accordance with the Bank for International Settlements, stablecoins nonetheless account for simply 1.5% of whole U.S. deposits, however progress is accelerating. “

A big-scale shift of funds from financial institution accounts into stablecoins might constrain banks’ means to fund new loans or lengthen credit score,” Morningstar analysts mentioned.

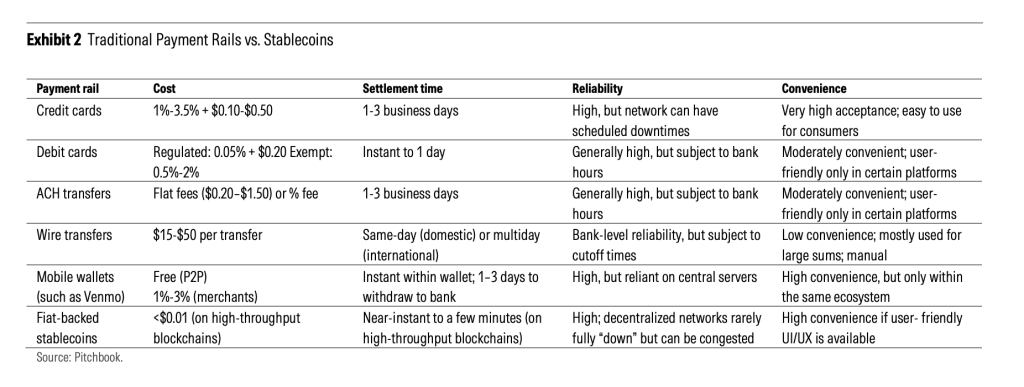

Banks additionally threat shedding profitable fee charges. Stablecoins bypass networks like ACH and SWIFT, enabling cheaper and quicker transfers. As Exhibit 2 reveals, the associated fee benefit is important, threatening income from transaction companies.

Not All Dangerous Information: A Path Ahead for Banks

Regardless of the dangers, Morningstar highlights potential alternatives. Banks might leverage their regulatory credibility to function custodians of stablecoin reserves, handle U.S. Treasury holdings, and supply settlement and compliance infrastructure. These companies might open new price revenue streams.

The newly passed GENIUS Act (Guiding and Establishing Nationwide Innovation for U.S. Stablecoins Act) units capital and reserve necessities for issuers, making a extra degree taking part in area. Some banks are contemplating launching their very own absolutely backed stablecoins, built-in into current compliance methods, to retain deposits and keep aggressive.

“Whether or not stablecoins finally signify a possibility or a risk to U.S. banks will rely on regulatory design and market adoption,” Morningstar concludes.

The put up Stablecoins Threaten to Disrupt U.S. Bank Deposits and Payments, Morningstar DBRS Warns appeared first on Cryptonews.